Your Financial Bunker: Life Insurance

H

aving a plan for the long-haul must be taken very seriously, and no retirement is complete without one. For many of you, the idea of life insurance might seem surprising (especially the concept of permanent life insurance), and I don’t blame you because the ‘80s and ‘90s saw a thriving stock market, more guaranteed pensions, and bigger Social Security checks, which all meant that clients from that generation weren’t as interested in life insurance. “Buy term and invest the difference,” was the mantra of the day. However, today, the stock market is more volatile, pensions are disappearing like dinosaurs, and Social Security is in the throes of upheaval! Retirees want and need guarantees. In retirement, life insurance can solve a number of issues. First of all, as a death benefit, it can transfer wealth to children for pennies on the dollar, allowing the parents to spend their money without worry. As a source of tax-free income, it can be a great supplement to retirement income. It can be an emergency fund or part of a plan to weather stock market declines if the client is using a portfolio withdrawal strategy. Term insurance doesn’t work well in retirement because the premiums increase significantly as people age. They are actuarially created to lapse before they ever pay a death claim (which is why less than 2% of term policies ever pay a death claim)! Let me explain some types of permanent life insurance very simply, and I’ll even tell you how to spot clients who suite each one.

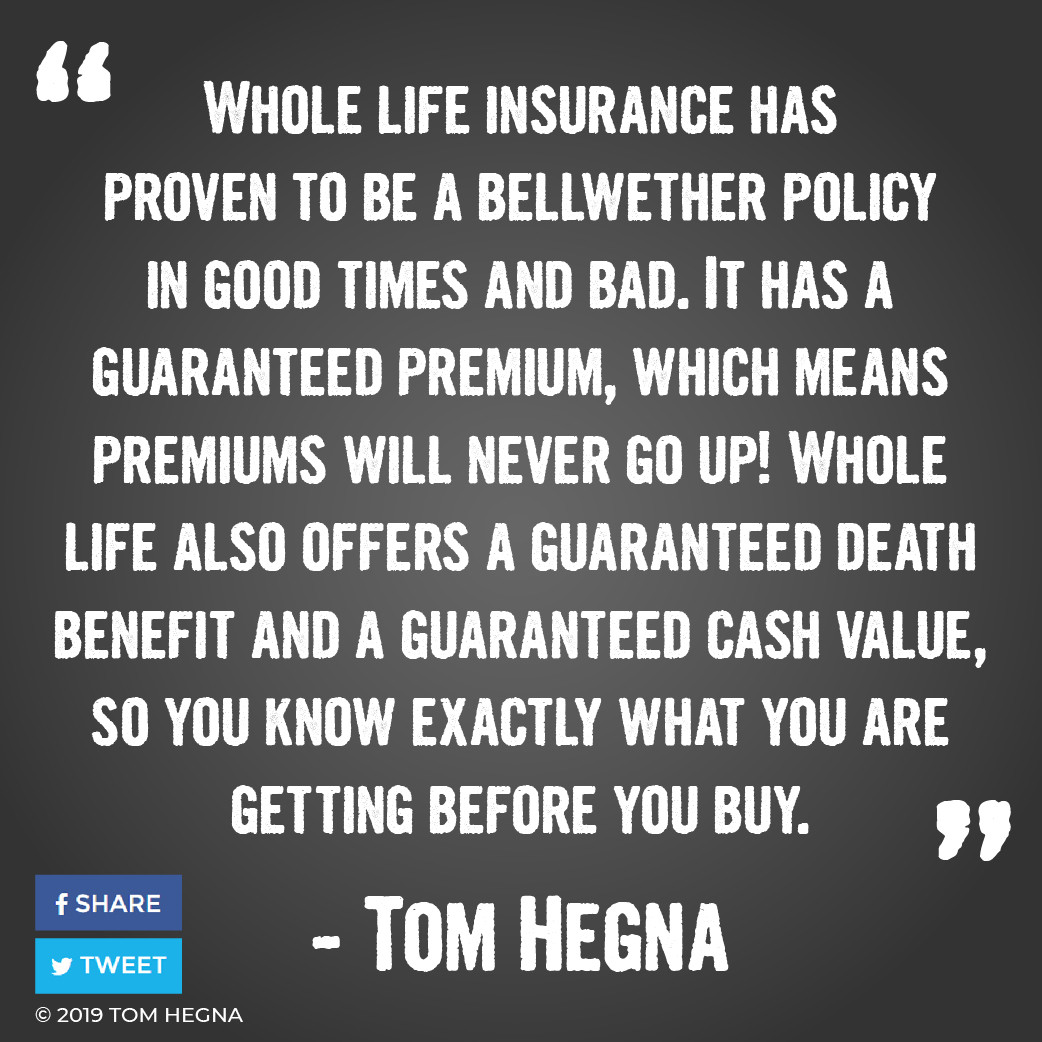

Whole life insurance has proven to be a bellwether policy in good times and bad. Market trends shouldn’t deter clients from this type of permanent life insurance. It has a guaranteed premium, which means premiums will never go up! Whole life also offers a guaranteed death benefit and a guaranteed cash value, so you know exactly what you are getting before you buy. What people typically don’t like about whole life is that they think they have to pay premiums for their WHOLE life! That’s why it is so important to at least show them a 10 pay or other limited pay policy. When people see this, they change their minds very quickly! Whole life has been used to build wealth by wealthy people for over a century. Walt Disney, JCPenney, and many others have used whole life to start multi-billion dollar businesses. This type of permanent life insurance is probably well-suited for clients who really want structure in their policy because it is full of the magic word: guarantees! It is for your most stable and reliable clients. There isn’t the same amount of flexibility in whole life. Premiums must be paid or the policy can lapse. The longer a policy is in force, the more flexibility it has, but this policy is really for people who understand the long-term advantages. Whole life insurance is more than just a forever-brand of term life insurance; it is a whole different animal because it does more than just provide a death benefit—it has guaranteed living benefits too! In fact, most types of permanent life insurance do.

Whole life insurance has proven to be a bellwether policy in good times and bad. Market trends shouldn’t deter clients from this type of permanent life insurance. It has a guaranteed premium, which means premiums will never go up! Whole life also offers a guaranteed death benefit and a guaranteed cash value, so you know exactly what you are getting before you buy. What people typically don’t like about whole life is that they think they have to pay premiums for their WHOLE life! That’s why it is so important to at least show them a 10 pay or other limited pay policy. When people see this, they change their minds very quickly! Whole life has been used to build wealth by wealthy people for over a century. Walt Disney, JCPenney, and many others have used whole life to start multi-billion dollar businesses. This type of permanent life insurance is probably well-suited for clients who really want structure in their policy because it is full of the magic word: guarantees! It is for your most stable and reliable clients. There isn’t the same amount of flexibility in whole life. Premiums must be paid or the policy can lapse. The longer a policy is in force, the more flexibility it has, but this policy is really for people who understand the long-term advantages. Whole life insurance is more than just a forever-brand of term life insurance; it is a whole different animal because it does more than just provide a death benefit—it has guaranteed living benefits too! In fact, most types of permanent life insurance do.

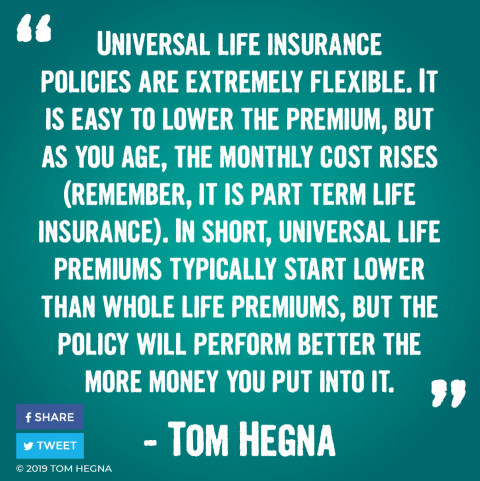

Universal life insurance is really a permanent life insurance policy that combines a term policy with a tax-deferred investment account. This account can be a fixed account, fixed index account, or variable account. The investment and interest rates go up and down based on market rates, but you get to maintain control of your premiums. With indexed universal life, you get a portion of the upside of the market, but you won’t see negative returns. Most policies have a minimum interest rate of 1% or 2%, even if the market is negative. With universal life, you can raise your premiums to save more, lower your premiums within the guidelines of the contract, and even stop your premiums as long as there is enough cash value to keep your monthly life insurance and administrative costs covered. Universal life insurance policies are extremely flexible. I have seen firsthand how powerful this flexibility can be. If someone loses a job, they can stop paying premiums for a while and then restart once they are back to work. I have even seen businesses saved by the loan provision of the policy. However, I have also seen the flexibility of these policies allow people to hurt themselves. It is easy to lower the premium, but as clients age, the monthly cost rises (remember, it is part term life insurance). In short, universal life premiums typically start lower than whole life premiums, but the policy will perform better the more money you put into it. If clients want the flexibility to boost their living benefits, universal life insurance can be a good fit, but the more flexibility a policy has, the greater the risks become.

Universal life insurance is really a permanent life insurance policy that combines a term policy with a tax-deferred investment account. This account can be a fixed account, fixed index account, or variable account. The investment and interest rates go up and down based on market rates, but you get to maintain control of your premiums. With indexed universal life, you get a portion of the upside of the market, but you won’t see negative returns. Most policies have a minimum interest rate of 1% or 2%, even if the market is negative. With universal life, you can raise your premiums to save more, lower your premiums within the guidelines of the contract, and even stop your premiums as long as there is enough cash value to keep your monthly life insurance and administrative costs covered. Universal life insurance policies are extremely flexible. I have seen firsthand how powerful this flexibility can be. If someone loses a job, they can stop paying premiums for a while and then restart once they are back to work. I have even seen businesses saved by the loan provision of the policy. However, I have also seen the flexibility of these policies allow people to hurt themselves. It is easy to lower the premium, but as clients age, the monthly cost rises (remember, it is part term life insurance). In short, universal life premiums typically start lower than whole life premiums, but the policy will perform better the more money you put into it. If clients want the flexibility to boost their living benefits, universal life insurance can be a good fit, but the more flexibility a policy has, the greater the risks become.

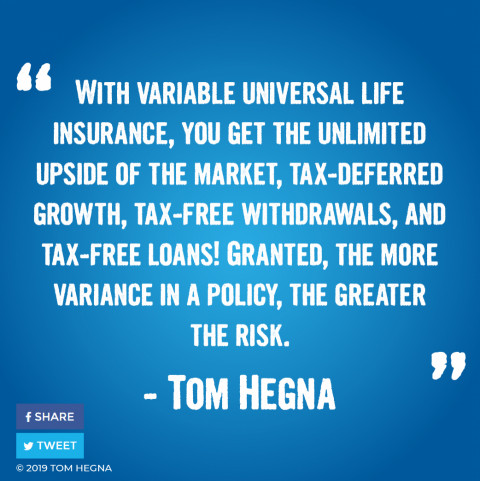

Variable life insurance comes in two flavors—variable whole life and variable universal life, but variable whole life is almost non-existent in the industry today. Variable universal life was very popular in the 90’s and has performed very well over time. With variable universal life insurance, you get the unlimited upside of the market, tax-deferred growth, tax-free withdrawals, and tax-free loans! Granted, the more variance in a policy, the greater the risk, so be sure to look at your client’s risk tolerance if they are asking about this type of permanent life insurance. This policy is great for people who say they want to buy term and invest the difference. By using variable life, all of their term costs count towards the cost basis of the policy. So they are actually getting tax-favored term life insurance that they would not get if they just bought a term policy on their own.

Variable life insurance comes in two flavors—variable whole life and variable universal life, but variable whole life is almost non-existent in the industry today. Variable universal life was very popular in the 90’s and has performed very well over time. With variable universal life insurance, you get the unlimited upside of the market, tax-deferred growth, tax-free withdrawals, and tax-free loans! Granted, the more variance in a policy, the greater the risk, so be sure to look at your client’s risk tolerance if they are asking about this type of permanent life insurance. This policy is great for people who say they want to buy term and invest the difference. By using variable life, all of their term costs count towards the cost basis of the policy. So they are actually getting tax-favored term life insurance that they would not get if they just bought a term policy on their own.

Overall, permanent life insurance provides guarantees that create retirement security in turbulent times like today’s markets. Explain this type of life insurance to clients as their financial bunker that can provide safety during difficult financial times. It is not meant to be a speedy, risky investment to gamble with. But it also doesn’t completely restrict liquidity like many talking heads would have you think. Just be sure your client understands that the more flexibility you want, the more risk you are taking on, but there is still more retirement security in the life insurance industry than the markets.

Overall, permanent life insurance provides guarantees that create retirement security in turbulent times like today’s markets. Explain this type of life insurance to clients as their financial bunker that can provide safety during difficult financial times. It is not meant to be a speedy, risky investment to gamble with. But it also doesn’t completely restrict liquidity like many talking heads would have you think. Just be sure your client understands that the more flexibility you want, the more risk you are taking on, but there is still more retirement security in the life insurance industry than the markets.

See you after your next appointment,

Tom Hegna